Intelligent Liquidity Optimization: Helping banks cut through the headwinds from SVB’s collapse and future liquidity crises

By Will Towning

Tremors have been felt across the global banking system following SVB’s collapse on March 10, with parts of both the U.S. and European banking sectors undergoing uncertainty and assessing contingency plans. Where the dust will eventually settle is hard to know. But with the pinch already being felt from higher interest rates and uncertain economic conditions, banks are bracing for another challenging period ahead.

There are several important risk management lessons being shared across the airways, but this article does not aim to repeat or contribute to them. Instead, it aims to explain how liquidity optimization and real-time liquidity analytics are now critical tools to help banks reduce costs, cut through the current headwinds and maintain Board and public confidence.

Liquidity buffers are akin to huge unrealized revenue potential

The largest banks in the world hold billions worth of HQLA – between $150 and $600B* – as a safety net for rainy days. As a rule of thumb, roughly one quarter of this covers intraday liquidity needs. While the current turmoil critically underscores the importance of effective risk management and the need for safety nets, advances in technology now enable banks to significantly and safely reduce these intraday liquidity buffers.

FNA is driving this innovation and helping banks unlock the huge unrealized revenue potential trapped in liquidity holdings. Our software offers the only effective liquidity optimization solution on the market, deploying advanced network science and simulation technology to help banks both optimize liquidity usage and provide the ever-more critical real-time analytics and stress-testing capabilities.

*(Vanderpool, Cheung “Largest banks reveal liquid capacity to take on Fed’s unwinding balance sheet)

ILO: Optimizing liquidity usage and needs

FNA’s ILO solution integrates into the real-time payment messaging flow of a bank. It hosts a set of powerful algorithms that identify and execute the timing and resequencing of payments that minimize liquidity usage. The solution enables banks to operate with an optimal amount of liquidity throughout the day, while also learning from and responding to stress events. By reducing intraday liquidity peaks, FNA’s algorithms also reduce risk and allow banks to effectively substantiate the reduction of their intraday stress buffers to their regulators.

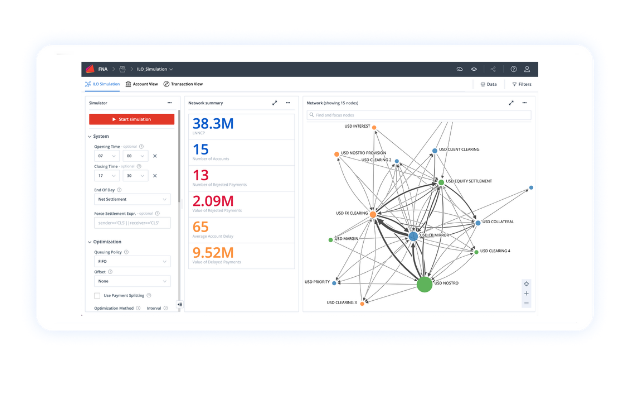

FNA’S ILO Software

ILO: Real-time analytics and stress testing

FNA’s ILO solution also provides banks with real-time analytics on liquidity and positions, as well as rapid stress testing capabilities. Our analytics and stress testing are further enriched by the fact that FNA maintains “digital twins” (replicas) of many of the world’s leading payments market infrastructures in our software, given our decades of work with them. The current market turmoil underscores the criticality of having such tools to respond nimbly to emergencies and take swift, informed decisions.

Further, FNA’s ILO solution also helps banks quantify and price liquidity risk more accurately, in addition to optimizing the underlying liquidity drivers. The combination of these capabilities provides banks with both a strong stance against the current headwinds as well as for when conditions rebound.

Network science and simulation are now critical tools for banks, FMIs and regulators

Financial networks are all around us. We are part of them when we make payments, borrow money or invest in financial markets. The actions that we take affect not only our own risks and rewards but also those of our direct counterparties and of everyone who is part of the same network of interactions.

Network science enables us to understand how these interconnected networks function as complex adaptive systems, which is invaluable when making investment and risk management decisions, optimizing payment flows and building measures to protect our systems from collapse.

Network simulation is another critical tool which helps us understand complex dynamics in modern financial networks. Simulations provide a laboratory setting, wherein one can analyze the probable effects of different system designs, disrupted payment flows or liquidity shortages.

Importantly, simulation models can be built to replicate the actual operating environment and can be used for stress testing and observing scenarios that are not normally found in real operating environments. This capability is invaluable when studying different crisis scenarios and evaluating how to best prepare for, and mitigate against them.

For Treasury managers, network science and simulation are unlocking new potential:

Simulation-driven algorithms using complex, proven heuristics for liquidity optimization

Complete visibility of payments and user networks to simplify management and oversight

The ability to run rapid what-if scenarios and stress test payments and user networks underscored by digital twins of the world’s important market infrastructures

Early warning indicators of changes in market and consumer behaviour with network-based anomaly detection

To understand more about how FNA’s ILO solution can optimize liquidity usage, provide real-time analytics and stress testing capabilities, please get in touch.