Macro-Prudential Porfolio Analytics

Dynamic Graph analytics for micro- and macro-prudential supervision

Mapping, monitoring, and examining the intricate relations between issuers and investors presents a profound challenge for financial supervision.

Fragmented data obscures the true nature of counterparty and liquidity risk. Without a clear view of how investors and issuers interconnect, authorities cannot accurately assess systemic importance or identify the cascading contagion channels that threaten market stability.

Macroprudential Portfolio Analytics provides a robust, flexible platform to supervise the intricate relations between issuers and investors with unprecedented detail.

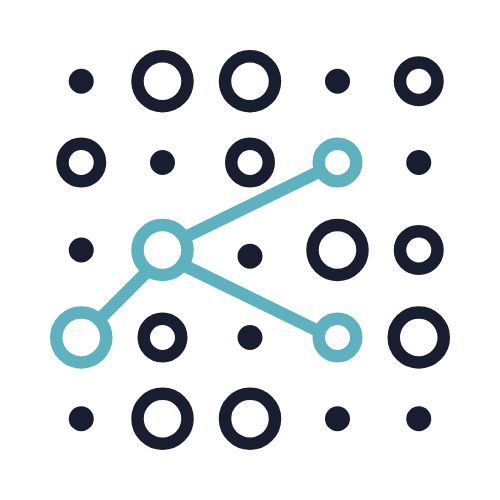

By consolidating multi-dimensional data into an interactive network graph, the platform provides a quantitative discovery of counterparty and liquidity risk. This enables authorities to safeguard the efficient functioning of financial markets and preserve overall financial stability.

Interactive Contagion Mapping: Visualizes the intricate and dynamic network of issuers, holders, and financial assets to make counterparty and liquidity risks fully observable.

Systemic Importance Quantification: Quantifies the systemic importance of specific holders and issuers, presenting different layers of risk in a readily available format for investigation.

Multidimensional Data Consolidation: Generates interactive dashboards from vast amounts of granular data from different sources (e.g., regulatory reports, live data from financial market infrastructures), covering all financial markets from savings accounts to equity and derivatives.

Dynamic Monitoring and Alerts: Leverages granular portfolio data to implement online monitoring and alerts, proactively identifying potential sources of liquidity risk.

Supervisory Reporting Analytics Use Cases

Uncover hidden investment vulnerabilities to mitigate counterparty risk

Map the complex interconnections between investors, issuers, and financial assets across all markets. This enables supervisors to pinpoint exact channels of counterparty and liquidity risk, revealing how localised stress can cascade through global investment networks

Quantify the systemic footprint of individual market participants

Evaluate the systemic importance of both financial and non-financial institutions based on the connectedness they create by issuing or holding securities and other liabilities (e.g., deposit accounts, time deposits). This quantitative assessment provides authorities with the precise, defensible data required to design and deploy targeted macroprudential policies.

Enhance crisis response with visual contagion mapping

Use interactive graph analytics to model and visualize the knock-on effects of market shocks. By making complex liquidity risk and contagion channels observable, authorities can rapidly communicate threats to coordinate defensive policy measures with key stakeholders during market stress scenarios.

Gain unprecedented insights into issuer and investor networks

Get in touch with the team to learn more about how FNA can help your organization visually discover contagion channels and preserve financial market stability

-

The platform consolidates multidimensional data from different sources covering a wide range of assets, including savings and current accounts, bonds, equity, and derivatives, providing a comprehensive view of financial markets.

-

Yes. The platform continuously monitors the investment portfolios of both financial and non-financial institutions to identify all potential sources of counterparty and liquidity risk.

-

By making the different layers of counterparty and liquidity risks, and potential contagion channels, observable and readily available, it significantly enhances decision-making in both normal and extreme market stances.