Why does payment throttling fall short of liquidity optimization?

By Jeremie Feuillette (Managing Director, Global Head of Liquidity Optimisation Solutions)

What is payment throttling?

Payment throttling refers to the process of limiting the rate of payments processed by a system. It is a simple rules-based mechanical solution. Some common techniques for payment throttling include:

Fixed-rate limiting: This involves setting a fixed number of payments that can be processed per unit of time (e.g. per second or per minute)

Dynamic rate limiting: This involves adjusting the rate of payments processed based on the current system load, congestion, or other factors

Burst limiting: This involves allowing a temporary increase in the payment processing rate, followed by a reduction to prevent overloading the system

Queue-based throttling: This involves adding payments to a queue and processing them in order, with the rate of processing limited by the size of the queue

Token bucket: This involves issuing a limited number of tokens that represent the right to process payments. Once all tokens have been used, the rate of payment processing is limited until more tokens become available

These techniques can be used alone or in combination, depending on the requirements of the payment system.

Negatives often outweigh the benefits

Reviewing the above techniques, it is clear that payment throttling can potentially lead to less liquidity risk as it reduces the potential of overloading the payment system and can limit credit facility usage. However, it also results in slower processing times, delayed payments and bottleneck payments. In some cases, this can lead to internal or external system gridlock.

These drawbacks naturally have negative repercussions on a bank’s customer satisfaction. Given this, can we really consider throttling an effective, long-term method for achieving improved liquidity consumption and liquidity risk? Regardless of where one stands on this, we must carefully consider the benefits and drawbacks of payment throttling and strike the right balance between reducing costs and delaying payments.

FNA’s Intelligent Liquidity Optimization: benefits without the drawbacks

FNA’s Intelligent Liquidity Optimization (ILO) manages this fine balance between liquidity usage and delays by intelligently resequencing payments, providing the benefits of reduced liquidity costs while also carefully calibrating and managing any payment delays.

FNA’s ILO solution leverages multiple synchronized Liquidity Saving Mechanism (LSM) algorithms for optimization along with network analytics for monitoring and understanding system dynamics. The LSM algorithms are used in the world’s largest wholesale payment systems and financial market infrastructures to provide the optimal resequencing of payment and minimize both liquidity usage, including LNNCP, and payment delays. The solution integrates bank and corporate real-world constraints, such as max LNNCP, max outflow/throughput, DVP, PVP, client pooling/netting, max overdraft and facility limit, and the inclusion of priority payment (margin call) and client SLAs.

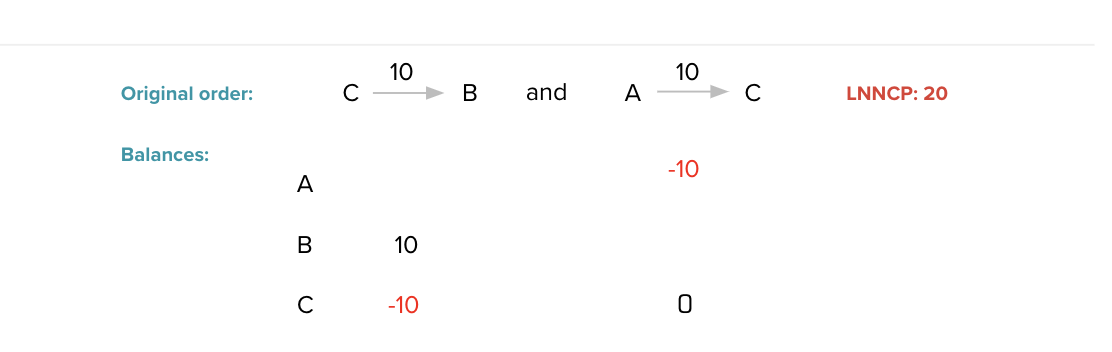

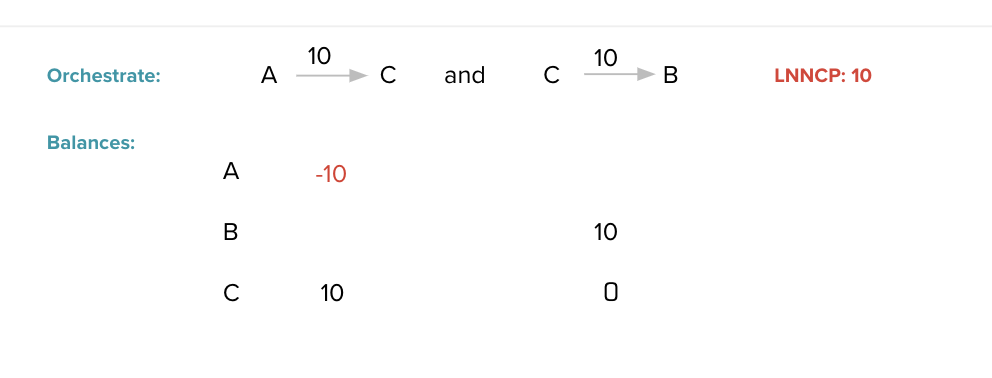

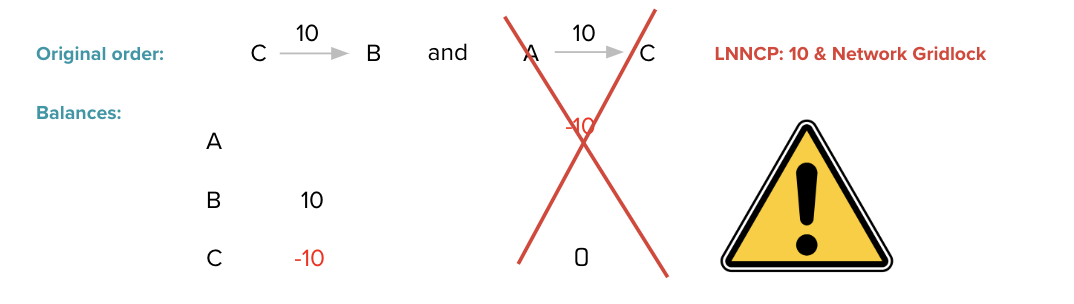

Let’s go through a simple example of 3 accounts and 2 payments to understand the differences between optimization and throttling. In this example, we assume that we want to have a Max LNNCP (overdraft for simplification) of 10:

1.Baseline: Two payments between three accounts in classic FIFO result in a total LNCCP (overdraft) of 20 and no payment delays.

2. Optimization with FNA’s ILO: The same two payments but now in a different order reduces the LNCCP by 50%, from 20 to 10, and also does produce only limited delay.

3. Throttling: despite the same two payments as the above two scenarios, throttling would result in a gridlock situation due to the overdraft limit being already reached. Thus would result in payment delays and unsatisfied customers (internal or external), in addition to being subject to potential technical default/ insolvency.

In a real-world setting, the volume and value of transactions and accounts are huge. The negative impacts of throttling on payment delay, gridlocks and customer satisfaction are also significant and difficult to manage from a bank operations perspective.

Can optimization and throttling cohabit?

Yes, throttling can be useful as a secondary control during black swan events, such as market crashes or major geopolitical instability.

However, the benefits of prioritizing intelligent optimization and resequencing of payments are clear.

For further information on FNA’s ILO solution, please visit https://fna.fi/solution/intelligent-liquidity-optimization/