From RTGS Simulation to RTGS Digital Twins – Why are they more powerful?

By Dr. Carlos Leon ( Director of Central Banks and Financial Market Infrastructures) and Dr. Kimmo Soramäki (Founder & CEO) & Adam Csabay (Head of Central Banking Engagements)

For decades, simulation has been an indispensable tool for understanding and optimizing Real-Time Gross Settlement (RTGS) systems. Researchers, policymakers, central banks, and financial market infrastructures have used simulation models to study the dynamics of liquidity, settlement efficiency, systemic risk, and policy design in RTGS and other payment systems.

Today, however, the field is undergoing a quiet revolution: the rise of digital twins. These virtual replicas of real systems are built not only to analyze the past or test theoretical ideas, but to interact with live infrastructure, guide real-time decision-making, and future-proof RTGS systems.

This shift is more than technological. It signals a fundamental change in how payment systems are understood, governed, and evolved.

Simulation: A Proven Tool for Payment System Insight

Simulation has a long and rich tradition in financial market infrastructure research. Because payment systems comprise a large number of interacting participants whose collective behavior is non-predictable at the individual level, with non-linear outcomes (i.e., they are complex systems), simulations powered by advanced financial network analytics have been the only way to analyze them quantitatively.

From early liquidity models to agent-based simulations of RTGS behavior, the ability to create synthetic payment environments has allowed central banks, financial market infrastructures, and academics to explore questions that cannot be answered through observation alone.

Seminal works in the 2000s used simulation to test the effects of liquidity-saving mechanisms (LSMs), settlement delay penalties, default scenarios, and topological resilience. These models helped answer critical policy questions: How much liquidity is enough? What happens when a large participant fails? How does tiering affect systemic risk?

Many of these studies, often powered by tools such as the Bank of Finland Payment System Simulator (BoF-PSS2) or later platforms developed at FNA, used synthetic or observed transactional data and ran as episodic exercises, producing valuable but static insights. They provided snapshots rather than continuous engagement.

The Emergence of Digital Twins

Enter digital twins: a next-generation modeling paradigm that retains the analytical power of simulation but is capable of integrating real-time transactional data, live feedback, and interactive interfaces. In essence, a digital twin is a living simulation—a virtual copy of the payment system that mirrors its real-world counterpart in structure, behavior, and data flow.

A digital twin of an RTGS system, for example, might ingest real-time transaction data, replay historical days, model hypothetical outages, or simulate policy changes—all while providing stakeholders with dashboards, alerts, and performance benchmarks. Rather than existing as a standalone model, a digital twin becomes part of the operational, risk, and Supervisory Technology (Suptech) toolkit of RTGS operators and their overseers.

Organizations like Payments Canada, the Bank of England, the Saudi Central Bank, and CLS have already adopted digital twins through partnerships with simulation technology firms like FNA. These twins are being used to guide system upgrades, test new settlement cycles, evaluate design alternatives, and support regulatory compliance.

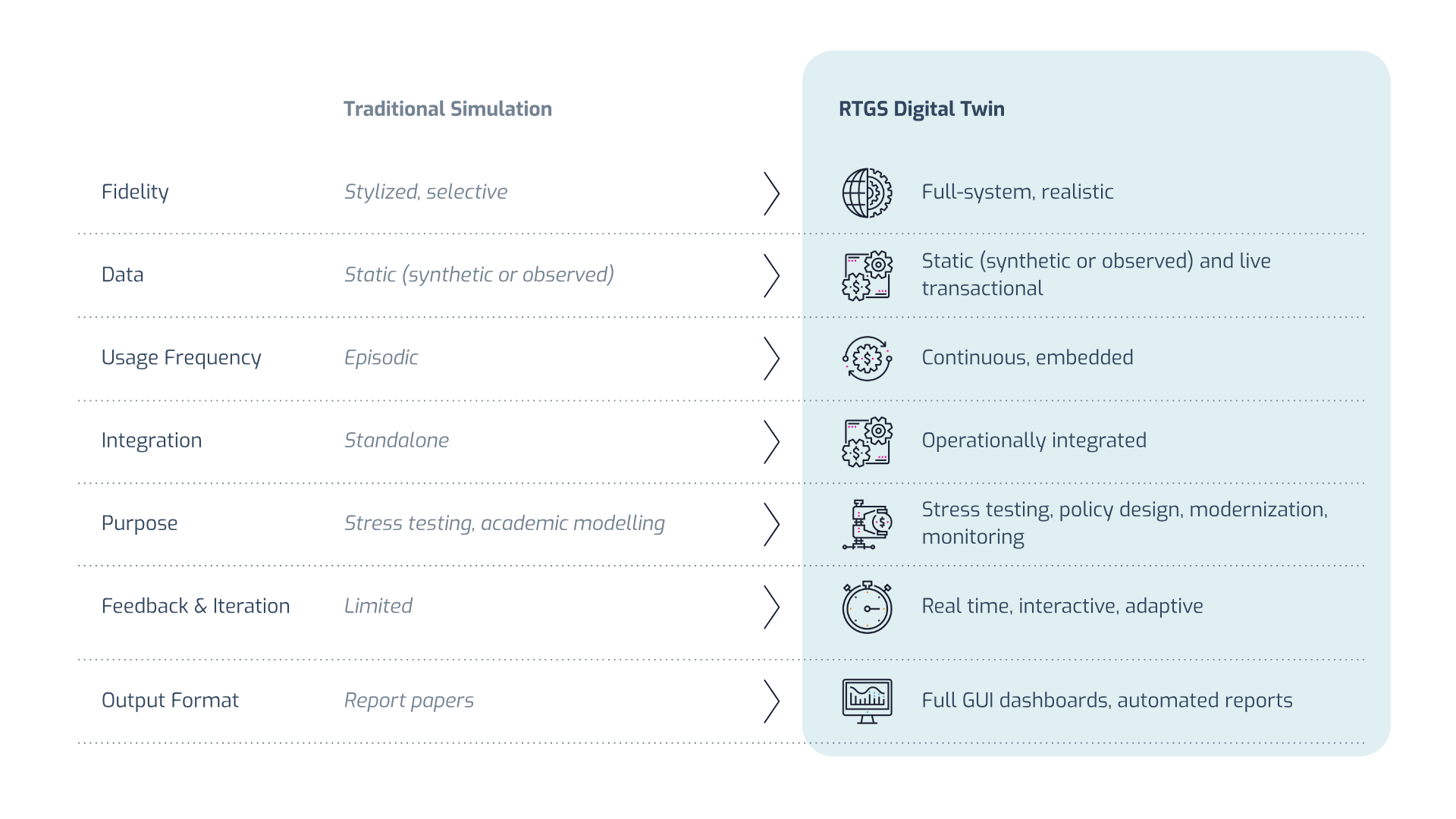

Key Differences Between Simulations and Digital Twins

While simulation and digital twins share common roots, their differences are significant. The following table summarizes the main differences between traditional RTGS simulation and RTGS digital twins:

Key Differences Between Simulations and Digital Twins

While simulation and digital twins share common roots, their differences are significant:

Scope and Frequency:

Traditional simulations are often one-off or episodic. Digital twins, in contrast, are always-on platforms designed for repeated, real-time use. They support ongoing monitoring and iterative scenario testing.

Data Integration:

Simulations rely on static and aggregated synthetic or observed transactional data. Digital twins are capable of integrating actual transactional data from the RTGS system, which is sometimes updated in real-time, allowing for greater fidelity and immediate applicability.

Operational Relevance

Simulations are typically research tools. Digital twins are embedded in policy and operational workflows, used to inform daily decisions, policy discussions, and crisis responses.

User Engagement

Simulation results are typically consumed through reports. Digital twins feature interactive dashboards, anomaly detection, and visual exploration, making insights accessible to broader audiences, including operations, policy, and oversight.

Extensibility

Simulations answer fixed questions. Digital twins can flexibly accommodate new modules, such as retail CBDC and stablecoins simulations, liquidity stress testing, or regulatory sandbox environments.

This table summarizes the main differences between traditional RTGS simulation and RTGS digital twins:

In short, digital twins are not just more advanced simulations—they are a transformation in how simulation is used and integrated into live systems.

The Road Ahead

The emergence of digital twins opens up exciting opportunities, but also raises new challenges. Among them:

Data governance must evolve to support the secure and responsible use of real-time payment data in digital twin environments.

Model calibration, validation, and auditability become increasingly important as twins begin to influence live policy decisions.

Scalability will be key, as central banks and financial market infrastructures seek to extend digital twins from RTGS to multi-system, cross-border, or even nationwide simulations that encompass banks, FMIs, and supervisory authorities.

At the same time, the benefits are profound. With digital twins, central banks and financial market infrastructures can:

Test policy before implementation, leveraging “learning-by-simulating” rather than “learning-by-doing.”

Detect and mitigate liquidity stress early using continuous Intelligent Liquidity Optimization (ILO).

Optimize operations and settlement efficiency.

Enhance communication with stakeholders, regulators, and overseers.

Perhaps most importantly, digital twins provide the tools to make financial infrastructure more resilient, transparent, and adaptable in an increasingly complex world.

Conclusion

The difference between simulation and digital twins is not merely technical—it is philosophical and strategic in nature. Simulations showed us what was possible. Digital twins show us what’s actionable.

As financial systems become increasingly interconnected and dynamic, building and maintaining a digital twin will no longer be a luxury but a necessity. The era of episodic modeling is giving way to a new paradigm of continuous, data-driven insights from simulation. The institutions that embrace it will be best positioned to guarantee the safe and efficient functioning of the payment system and lead in the future of payment system innovation.